Amid underlying volatility in wholesale power prices, opportunities for access to wider flexibility revenue streams, and the impact of price cannibalisation, the case for co-location for renewable energy assets is growing.

As part of Cornwall Insight’s Renewables Pipeline Tracker service, a case study is included in each report’s release based on a topical developments seen in the renewables pipeline or wider market. In our Q122 report (issued in June 2022), we provided a summary of known co-located sites currently in the development pipeline. In this blog, we explore the key trends from the case study.

Our June 2022 analysis identified a total of 217 sites in the development pipeline that are co-located with known sites in either our Renewables Pipeline Tracker or BEIS’s Renewable Energy Planning Database. This total has doubled in capacity terms, from 4.3GW (156 sites), since we last conducted the analysis in January 2021.

Based on the current co-location pipeline, there is a clear dominance of co-located solar PV and onshore wind projects. This is unsurprising given the impact of price cannibalisation—the depressive influence on achievable wholesale revenues at periods of high renewables output—that these technologies are subject to, alongside an increasing volume of older solar PV and onshore wind sites that may now be looking to extend their project lifespans. Solar PV dominates the co-located pipeline at 171 sites (8.7GW) in our June 2022 analysis, followed by onshore wind at 40 sites (2.6GW). This has increased markedly for solar PV, rising from 41 sites (970MW) as in our January 2021 analysis.

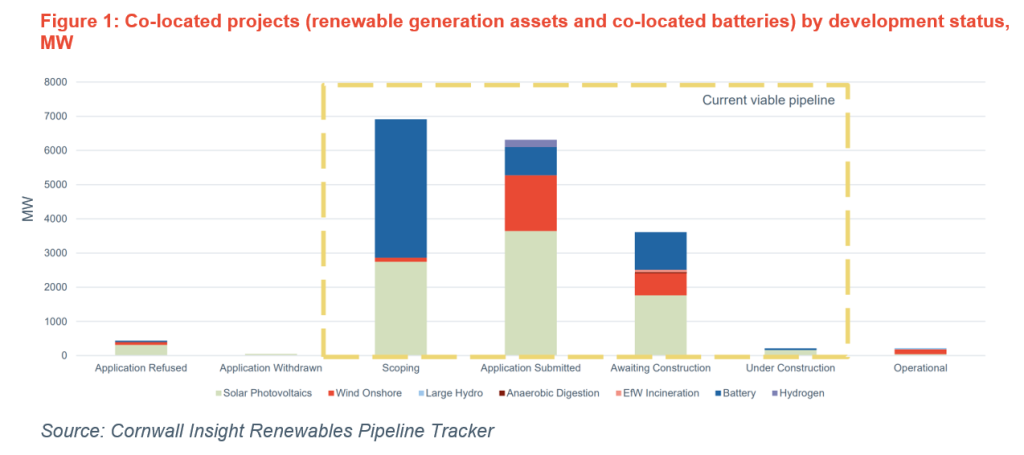

The majority of pipeline co-located sites (including associated co-located batteries) have a development status of either scoping, application submitted or awaiting construction, at 6.9GW, 6.3GW and 3.6GW, respectively, with a smaller amount (211MW) classed as under construction. A small proportion of sites, mainly onshore wind (141MW) are operational however, with their respective batteries currently in the planning pipeline. Importantly, the large amount of battery capacity (4.0GW) currently in scoping follows a trend of increasing capacity of new-build storage assets.

The number of planning applications submitted for co-located sites in recent years has increased sharply, with 157 projects submitting planning applications in 2021, and 63 to date in 2022. Additionally, for older projects there is a greater amount of time between the planning applications for the renewable energy asset and its co-located battery being submitted. This is in part due to a number of older extension and repowering renewable sites which have since added battery co-location to their project plans, in addition to a wholesale pricing environment that supports energy storage.

In contrast, there is a generally shorter period of time between each planning application being submitted for newer sites, with the majority of projects post-2018 being in the same year for both the renewable energy site and its respective co-located battery.

Whilst co-location is not without its challenges, the current volatility in underlying wholesale power prices indicates ample scope for future growth of co-located projects, with co-location allowing renewable energy projects to enter meaningfully into additional revenue streams, such as response services and the Balancing Mechanism, alongside further benefits such as shared grid connections and associated cost reductions.

The Renewables Pipeline Tracker service comprises a searchable, accessible database and accompanying analysis report, designed to provide detailed information on future renewables generation assets and transparency on the pipeline of assets coming to market. Updates are issued quarterly, with special feature case studies analysed to provide a detailed view on developments within technologies and types of asset. To find out more about the Renewables Pipeline Tracker, please contact Bertie Bagge b.bagge@cornwall-insight.com