Christmas 2021 was not a time of cheer for the energy industry and its customers. There is acute stress on energy suppliers and consumers from current bills – let alone where they may move to in the coming year. And it seems the political and regulatory debate has moved on from whether intervention might be justified to lower bills under the summer 2022 Default Tariff Cap when we broke for Christmas, to exactly how that intervention might be achieved and what form it should take.

Media reports have focussed on discussions between BEIS and suppliers, with references to the Treasury and potential costs of mitigation measures of up to £20bn (roughly £750/household). In addition, Ofgem is running short notice consultations on how and when the costs of supplier failures should be recovered, supplier conduct, changed approaches for pricing overall in the domestic market and potential changes to the structure of the Default Tariff Cap itself.

For domestic suppliers, the situation is compounding as virtually the whole market is migrating to the Cap as fixed tariffs either expire or become unaffordable and force companies from the market. With no relief in sight for wholesale prices, existing hedges rolling off and the Default Tariff Cap firmly in place, things get more and more unaffordable until the whole energy sector and the wider economy becomes exposed to systemic risk.

Minds seem to have been concentrated by the prospect of a near-doubling in the Default Tariff Cap by next winter. The supply industry, led through Energy UK, has been consistently arguing that the UK is experiencing an energy bill crisis that has the potential to develop into a full-blown fundamental economic challenge. Its message now seems to be being heard. There is also a growing realisation that we could see for some time yet the extreme wholesale market conditions that have been the cause of the current crisis.

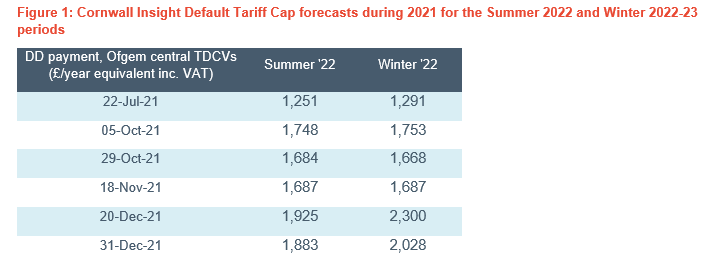

With a month to go before its wholesale pricing window closes for the Summer 2022 period, the level of the Default Tariff Cap from 1 April 2022 is now becoming baked in. Including an estimated £90/year costs for failed suppliers, the Default Tariff Cap looks like out-turning just shy of £1,900/year, an increase of 50% or so on the level currently in place until 31 March 2022. But there remains considerable volatility in where the Winter 2022-23 cap will land. The wholesale price window for the Winter 2022-23 cap will open from 1 February 2022, so the numbers in Figure 1 are indicative for now as they are based on forward curve snapshots on the dates the forecasts were made. But they do show the volatility in where the Default Tariff Cap may end up.

If the market continues as it ended in 2021, the Default Tariff Cap for Winter 2022-23 will rise a further 8% on Summer 2022 to a level of over £2,000/year. But the bad news is that the first trading sessions of the New Year saw the wholesale market rebound, implying a rise in the cap back up to the levels we forecast just before Christmas 2020.

This volatility underlines the challenge for anyone trading in this market and those who may be contemplating interventions to mitigate the immediate impact of the higher costs on consumers. Though action may limit the immediate impact, any measures will still need to be paid for. Critical questions will be by who and over what time period?

In this regard, Ofgem’s 29 December consultation on third party financing for the costs of Supplier of Last Resort (SoLR) failures may show some straws in the wind. It proposes to create a financial special purpose vehicle (SPV) to borrow money covering the SoLR claims from banks. The SPV would then buy the SoLR liabilities from the suppliers that took on the SoLR customers, including the right to recover the net costs over time from licence-driven obligations on network costs. Some £1.8bn of costs have been incurred under SoLRs to date. Our £90 forecast for the costs of failed suppliers for the Default Tariff Cap assumes recovery in one financial year, so one would assume that using an SPV to spread the costs over time would reduce the unit costs for next year proportionately but extend consumers’ liability over time.

Ofgem’s proposal outlines some of the parameters of the choices available to limit the immediate impacts on energy bills. These choices concern the routes to, source of and nature of support. Cornwall Insight’s Senior Consultant Dr. Craig Lowrey fleshed out some of the options available with the potential to reduce bills in the short term. As Craig set out, mitigating the full £700/year or so rise from 1 April 2022 in the Default Tariff Cap could entail measures deferring policy, network and VAT costs, or virtually every major lever outside the wholesale market. Alternatively, a means to defray these wholesale costs could be put in place. In terms of funding, grants or public or private sector loans may be options. Media reports over Christmas suggested the Treasury is uncomfortable with £20bn cost mitigation measures apparently sought by the industry.

There are then questions about who should be the recipients of support to mitigate their energy bills next summer and how should it be made? Many householders will find paying the extra £700/year a big stretch, but are the costs involved so large that only targeted support can be afforded? This looks like a big political choice, as is the extent to which support might be extended to businesses, especially those who have had their opportunities cut due to COVID-19. What should be the route of the support? Here there are many choices, again with a heavy political weighting, including:

- Direct relief to consumers (for example through the tax system, Winter Fuel Payments, Cold Weather Payments or Universal Credit). Such payments could be targeted or made generally available but there may not be a guarantee that the money would be received by suppliers for fuel bills. If this is not the case, their bad debts could increase leading potentially to more socialised costs if more companies are forced from the market.

- Payment to or cost mitigations for suppliers to be passed on to consumers (for example through a VAT holiday or loans or grants to fund increased Warm Home Discounts or network costs). Depending on the route this mitigation takes, it also allows targeting of support but again increased credit risk and potential for more mutualised costs if more suppliers fail and they are unable to repay funding made through loans.

- Grants to service providers funded by government or private sector loans. Such payments could be made to cover the costs of networks, renewables or even fossil generators facing very high purchase costs. They would mitigate the costs to be recovered through bills this summer, but would be difficult to target support compared with some of the other measures outlined above. Also, this option carves those with better credit positions from the market, so maybe there could be value obtained for limiting the credit risk that these entities face from an unstable supplier base?

How could this also be paid for? Potentially in the wider tax base, and by doing so perhaps marking the start of a long-desired permanent shift for policy costs from bills, a loan recoverable through network charges (as with the supplier loan scheme from last winter and Ofgem’s proposed SoLR SPV) or loans directly recoverable from suppliers (but with the concerns as above on credit risk). There has been talk of a windfall tax, though such gains will be very hard to attribute and could unfairly penalise those GB energy producers who have done the prudent thing and sold ahead. However, the optics for renewables generators do not look good for high Roc recycling values on top of a very high forward curve.

It goes without saying there are a lot of big decisions here with the pressure on for them to be taken in very short timescales. If we want to continue with a competitive retail market, such fundamental choices should be based around the principle of where we want to end up, even if the pre-COVID normal may never return. Perhaps inevitably, BEIS has decided to park its retail development work into a wider call for evidence. This may be a recognition of overall priorities, but the original vision of this took some years to develop and needs to be returned to one day soon if we want to have an alternative to a world of capped retail prices.

An important question also needs to be added to BEIS’s headline list of questions for its call for evidence. To what extent does the wholesale market design drive consumer bills and thus incentives on suppliers? The answer is “wholly”, as those who tried to ignore the wholesale price element of the Default Tariff Cap formula have found to their cost.

Supplementary questions, alluded to by the recent Financial Times (FT) coverage of a proposal from suppliers for a Contract for Difference (CfD) style mechanism for wholesale costs as a whole, is to what extent the current wholesale market design is exacerbating the current situation and to what extent the outcome would be different under a different market design? As the FT piece implies, it is interesting that we are prepared to contract long-term for power at long-term prices (through CfDs) but for 30 years and more we have viewed such mechanisms for gas as a “bad thing”. But it is the marginal gas price that is driving the whole value chain in energy right now, and it looks like it will continue even as our dependency on fuel declines. Work to look at different ways of valuing wholesale energy needs to continue, but we should be wary of formula-driven mechanisms subject to changing political direction: one of the main arguments for privatising electricity was unwinding the last scheme for that purpose, the Bulk Supply Tariff of the Central Electricity Generating Board.

This work should be very important given Ofgem’s four Default Tariff Cap and Supplier Licensing Review consultations. Together they underline that the retail market fundamentals of the future will be very different from the past. The government and Ofgem have made it clear that the Default Tariff Cap is here to stay and suppliers will be expected to hedge to it with stability and growth tests. In the absence of further action, this – in combination with the wholesale market design considerations – will mean that consumer prices will become more tied to fossil fuels even as we reduce our dependence on them. This will up the political pressure that is now coming on the government to justify policy costs in bills. We have no answers as yet on an alternative, but we surely need to address this urgently as, even if the current situation passes relatively quickly, there will be a huge transfer of wealth from consumers to producers, and often out of the country.

These pressures mean it is very important that we keep in mind what the retail market is ultimately for. When the government legislated for the Default Tariff Cap, we switched from a view that engaged consumers to keep the supply side on its toes, to one where direct regulation of price is the vehicle for this. Unfortunately, many challenger suppliers either hoped this was really not the case or were unable to adapt their businesses in time for the first time the Cap and the market clashed. There are risks now that well-intentioned interventions for the short term will reinforce incentives and structures for years to come, in particular pricing for the very fossil-fuel dependency that we want to reduce and thus pressuring even further the decarbonisation subsidies so tightly wound into current bills.