In October 2020, National Grid Electricity System Operator (NGESO) implemented the soft-launch of the Dynamic Containment (DC) service, the first in a new suite of faster-acting frequency response services. Since its launch, the DC service has been the most lucrative response service and has grown considerably in the past year. The one-year anniversary of the service provides an opportunity to review its evolution over the past year.

Introducing faster frequency response services is critical to achieve the ESO’s ambition of operating a zero-carbon grid by 2025. As non-synchronous renewable technologies make up an increasing share of the generation mix, system inertia decreases, which in turn requires response services to respond quicker to manage frequency deviations. Participants in DC must provide response on timescales of less than one second. This sub-second response requirement favours battery assets, which so far are the only technology to participate in the service.

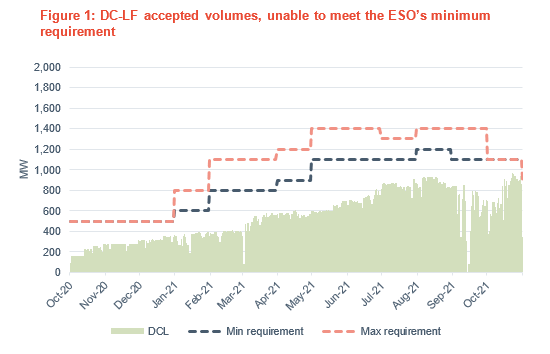

After launch, DC prices quickly settled at £17.00/MW/hr, a level the ESO determines provides better value than taking alternative actions. With an initial volume cap of 500MW, and average procurement at 190MW during October 2020, the service was notably undersubscribed. This theme has continued over the past 12 months, with growing volumes in the service unable to keep up with rising service requirement (Figure 1). More stringent technical requirements, namely 20Hz performance monitoring, has acted as a barrier for older battery assets to jump from the monthly Firm Frequency Response (FFR) service over to the more lucrative DC service.

Nonetheless, we have seen significant month-on-month growth in DC to average 880MW in August, before a drop in volumes over September due to the shift to EFA-block procurement. This has come at the expense of the FFR service, with both monthly and weekly FFR auction volumes falling considerably

since the introduction of DC.

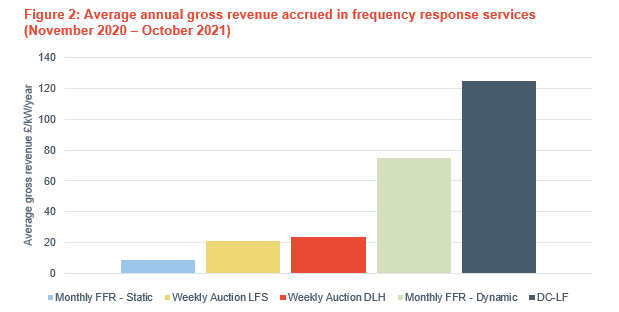

DC tender prices have remained at a premium to all other response services, with Dynamic FFR tender prices typically the second-highest ranging between £8.0-12.0/MW/hr. Figure 2 shows the gross revenue accrued in the DC service over the past 12 months (i.e. does not account for costs faced by an individual asset such as wholesale purchase costs), averaged across all active units. The average gross annual revenues of DC participants is £124.9/kW/year, with revenues of up to £149/kW/year available to participants active in the service for all hours of the year. Compared to revenues available in other frequency response services or for batteries in arbitrage, there has been a significant premium enjoyed by DC participants to date. Due to all parties bidding in at the same price point, higher revenue is currently associated with higher activity levels in the service. The parties who have accounted for the largest share of accepted service volumes to date, and therefore accrued the largest revenue, have all been active seen go-live.

The recent procurement changes, part of the ESO’s transition from a ‘soft launch’ to a full service, now mean DC is procured by EFA block, on a pay-as-clear basis. This shift is changing procurement characteristics, with the ESO’s recent Market Information Report suggesting there will be a 65% drop in requirement in November. As such, we anticipate the service becoming oversubscribed in November, with potentially over three times more supply outstripping requirement and prices easing from their £17.00/MW/hr stronghold. On 1 November, this was realised as prices fell to £14.90/MW/hr for EFA block 6, with a volume-weighted clearing price of £16.70/MW/hr across the day. This is the first time prices have cleared below £17.00/MW/hr since October 2020. As the service matures to competitive auctions with EFA block procurement, we expect to see greater price variation and volatility throughout the day. This was exemplified on the 2 November; average tender prices ranged from £1.59/MW/hr in EFA block 2 to £47.99/MW/hr in EFA block 5, with the ESO accepting DC bids over £17.00/MW/hr for the first time amid tight system conditions.

DC bids are stackable with bid-offer acceptances in the Balancing Mechanism (BM), as long as any BM activity does not compromise an asset’s ability to meet their DC obligations. This has enabled battery assets to access multiple revenue streams within-day since BM stacking was unlocked back in January 2021. Recent developments have accelerated this trend, with the shift to EFA block procurement facilitating within-day optimisation across different revenue streams. This was showcased across October during exceptionally high wholesale power prices, where we have seen lower procurement during EFA blocks 5 and 6 as assets withdrew to trade in the evening peak in wholesale markets or the Balancing Mechanism.

Looking forward, the high frequency product of the DC service (DC-HF), designed to manage the largest outfeed loss on the system, launched on the 01 November. Although the requirement is initially relatively low this winter, it is expected to grow into 2022 as the North Sea Link (the largest outfeed loss) is commissioned at full capacity and into the summer season where periods of low system inertia are more prevalent.

The roll-out of Dynamic Moderation and Dynamic Regulation is expected in March 2022. These pre-fault services are designed to complement DC and maintain frequency within operational limits (±0.2Hz). As these services go-live, the ESO will transition away from existing FFR services completely, to be replaced by the new response and reserve services.

We will be analysing and commenting on the latest developments in DC and the ESOs wider ancillary services in our monthly Flexibility Markets Report. For more information on this service please contact Tom Ross at t.ross@cornwall-insight.com.

You may also be interested in…

Flexibility markets report

This report provides key analysis of the commercial developments throughout the flexibility revenue streams across GB. Providing a collective view of value across all National Grid ESO and DSO flexibility markets, the report provides a monthly analysis of market forecasts and revenue benchmark and backcast assessments.