This Energy market perspective was taken from our Energy Spectrum publication on 4 October 2021. To find out more about a free trial to Energy Spectrum, find out more here or contact Robert on r.buckley@cornwall-insight.com.

As we enter the winter 2021-22 trading season, the energy supply market remains in intense distress as wholesale prices continue to soar. On Friday, the price of wholesale gas (October 21 contracts) reached 175p/th, up 50% compared to the end of August, while electricity increased 64% to £187/MWh. Even amid COVID-19 recovery and disruption elsewhere in the economy, the challenges this presents, alongside a raft of other costs going into the winter months, remain at the forefront of the national agenda.

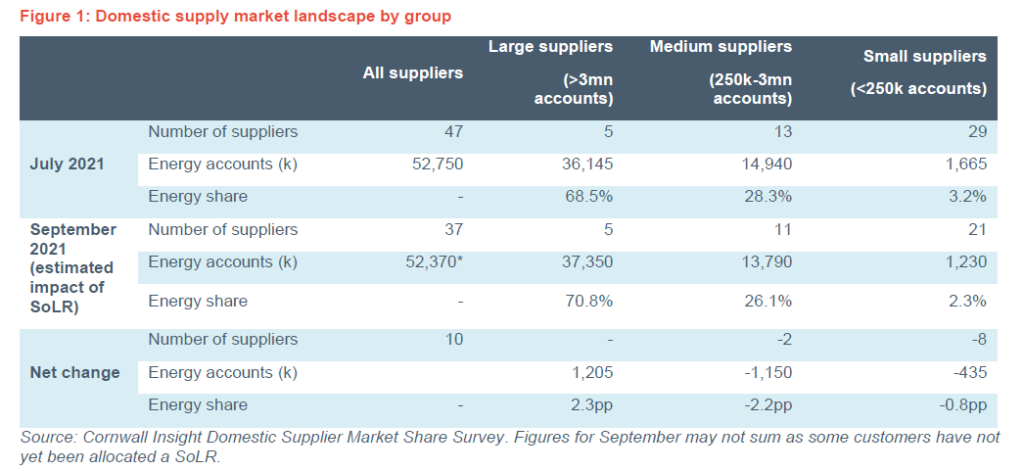

Consolidation across the domestic supply market has been an ongoing feature over the last four years, and in 2021 the number of active competitors has continued to decline. Since the start of the year, we have recorded 14 exits from the domestic supply market, nine of which have occurred in September. As Secretary of State Kwasi Kwarteng alluded to recently, this figure benchmarks close to previous years which ranged from nine to 13 exits a year since 2018. But unlike previous years, 12 of the exits have been through Ofgem’s Supplier of Last Resort (SoLR) mechanism, compared to around 40% that were trade sales previously.

Today, we count 37 licensed suppliers (alongside a raft of while label companies) operating in the domestic energy market (Figure 1). Five supply more than 3mn energy accounts, 11 between 250,000 and 3mn accounts while the balance supply fewer than 250,000 energy accounts. Many of the latter group are long-term competitors with a steady portfolio of customers, not seeking (or achieving) the scale of some of the recent-but-exited entrants. For many small suppliers, their scale is an active commercial choice, perhaps because they target niche consumer markets or sell particular energy sources.

The world is not enough

Some of the suppliers to exit the market have cited wholesale trading difficulties. Igloo Energy referenced the impact of the “short-term crisis” in wholesale prices, while Utility Point said the “perfect storm of events” had led to it cease to trade. Utility Point referenced the high wholesale price alongside the “increase in debt and deficit” caused by

Ofgem’s request to offer extended payment terms and lenient debt collection. The supplier also cited what it saw as the limitations of the Default Tariff Cap, which despite the increase in October, is “still over £200 below the cost to supply the energy”. Utility Point said it had been “impossible” to hedge in line with the way the price cap is calculated.

The recent round of exits has come with understandably emotive messages from business owners, many of whom were aiming to deliver change in a market that will experience substantial changes in consumption in the coming years. While most customer communications focused on key messages around continuing supply, some also acknowledged the difficult times ahead for their teams whose jobs are now at risk.

For the 7% of domestic energy customers impacted by SoLR this year (some potentially more than once if they switched, say, from Green Network Energy after its January 2021 exit to a more recent departure), there will be concerns over billing, credit balances, debt payments and the new prices they will now have to pay. Some of the failed suppliers offered the cheapest tariffs in the market, growing fast mainly through price comparison websites. Since the start of 2021, 38% of the cheapest tariffs available were offered by a now failed supplier (Tariff data from Comparison Technologies, weekly data using Ofgem medium TDCV for a dual fuel, direct debit customer). Assuming they move to a tariff at the winter 2021-22 Default Tariff Cap from fixed deals priced below £900/year, these customers will collectively face a bill of more than £100mn.

They will see few if any deals to switch away below the cap. While this may disappoint them, it also means that the acquiring suppliers under SoLR are taking the extra costs to market prices from the lower level of the Default Tariff Cap. Industry hearsay is that this cost could be £250/year for a typical dual fuel customer. We will get a clearer picture of where these costs ultimately land when Ofgem outlines the results of each of its SoLR switches so far, but we would be surprised if acquiring suppliers can absorb much of them. This opens the prospect of these costs being recovered from all other consumers through the SoLR levy.

Skyfall

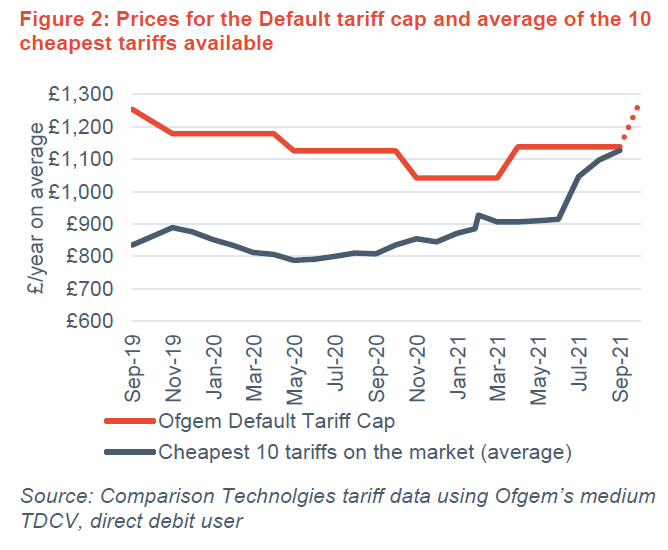

Domestic tariff prices have seen a noteworthy increase over the summer months. The cheapest 10 tariffs on the market in April averaged £906/year for a typical dual fuel user, while the equivalent figure stands at £1,127/year as of 27 September, an increase of nearly a quarter Figure 2 shows, with a consequent reduction in potential savings against the Default Tariff Cap. Given the market pressures, it is logical that the gap has closed. But it took longer to do so than those wholesale pressures suggest.

Wholesale prices have been on a rapid escalator since the end of last winter, but competition between the likes of PfP Energy, HUB Energy, Utility Point and Neo Energy during the Spring of 2021 limited those pressures in the domestic market. We saw similar trends in 2020, when now-failed Tonik Energy pitched low fixed price tariffs. Speculation is that this behaviour, when accompanied by month in advance payment, is suppliers seeking finance from their customers when other commercial sources are unavailable to them.

The sustainability of that competition will now be questioned harder than ever by consumers and policy makers. To date switching for domestic consumers has been presented as an easy and no-regrets option: do not worry if your supplier fails, your energy will flow and, implicitly, your tariff will not change much, if at all. That is not the case for many this time and it will be little consolation to those switched up to the Default Tariff Cap that their bills at market would be even higher. For the SoLR-acquiring suppliers, as well as the extra supply costs, this growth brings with it new challenges, with multiple other costs from data cleansing to communication costs, some of which can be recovered and some cannot. There is lots of speculation about the ability of remaining suppliers to absorb more customers. With the experience of 39 suppliers leaving the market through SoLR over the last five years, the industry is now much more familiar with the process.

The regulator acknowledges that the role of SoLR can “represent a significant logistical challenge” to a supplier, incurring increased administrative and energy purchasing costs. The SoLR mechanism allows acquiring suppliers to make a claim for the otherwise unrecoverable costs that they have incurred through a “levy” which is socialised back across customers through DUoS charges (see Figure 3). While Ofgem encourages suppliers towards not making a claim on the levy, there are least five cases of this occuring throughout the last two years, with ~£28mn claimed since 2020. Other costs, notably for policy schemes including the Renewables Obligation (RO), are also recovered from the market. We estimate there is pushing £200mn of defaulted RO costs alone for 2019-20 incurred by the supplier exits since that charging year started in 1 April 2019.

The scale of exits and fears that there are more and perhaps bigger to come has prompted fears of contagion and systemic risks. The media made much of Ofgem puting a “special administrator” on standby to manage a supplier whose failure might be too much for SoLR to absorb.

To continue reading…

For the full Energy market perspective, please request a free trial of Energy Spectrum below.