Tensions along the Russia-Ukraine border have been escalating since November last year when satellite imagery showed a fresh build-up of Russian troops on the Ukrainian border. Fast forward to the 24 February 2022, Ukraine and Russia are now at war following a Russian invasion. In response to these actions from Russia, the US, UK, and EU announced a series of economic sanctions and Germany announced that it would withhold approval for the Nord Stream 2 gas pipeline.

The ensuing conflict is a continuing humanitarian tragedy. We know that first and foremost these human impacts are the major issues arising from the conflict and our commentary on energy-related impacts are in no way intended to distract from that.

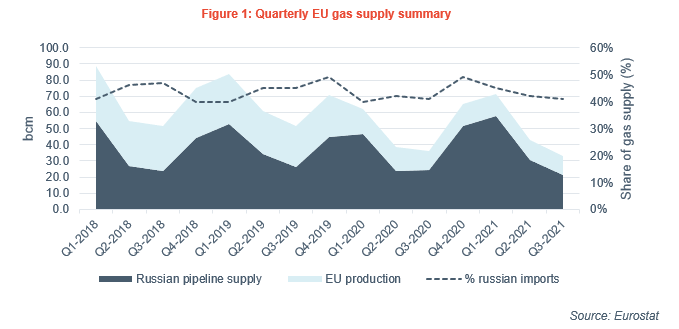

Dependence on Russian gas

Around 87% of all gas supply in Europe is imported, and Russia accounts for approximately 31% of total European supply while Russian LNG deliveries account for another 4% in 2021. This, as highlighted in Figure 1, shows that Europe is heavily dependent on Russia for its gas supply. Meanwhile, the Oxford Institute for Energy Studies (OIES) highlighted in a recent report the supply interdependencies between the UK, Norway and continental Europe via existing gas pipelines (interconnectors), namely with, Norway, Belgium, France and the Netherlands.

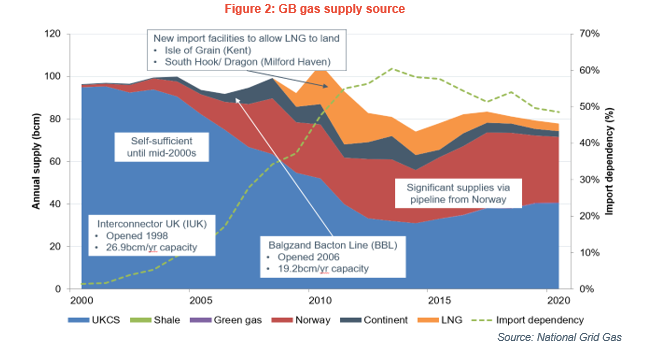

While around 40% of the UK’s gas is currently sourced from Norway (Figure 2), OIES noted the limiting factor for Norwegian supply is not pipeline capacity but Norwegian production, much of which also flows to continental Europe. Therefore, the UK could only receive more pipeline gas from Norway should those flows be diverted. Regarding our interconnection with Europe, gas generally flows to Europe in the summer to take advantage of the greater storage levels on the continent and flows to the UK in the winter.

Regarding our interconnection with Europe, gas generally flows to Europe in the summer to take advantage of the greater storage levels on the continent and flows to the UK in the winter. Overall, imports via interconnectors with continental Europe supplies approximately 5% of GB supply. Remaining gas supply into the GB system comes from the UK continental shelf (~40-45% of supply) and the remainder from LNG (~10-20%).

It should be noted that the UK’s relationship with Russian gas is far more muted than mainland Europe, with Russian imports only accounting for 4% of UK supplies in 2021. This is due to the UK having no direct pipeline connections with Russia, with supplies stemming from LNG deliveries alone. However, this far more limited exposure has not isolated GB from gas price rises as supply concerns continue to rise.

Security of supply and Net Zero

If Europe does face the scenario of a shortfall, the reaction and how supply issues are dealt with could have long lasting implications for the region’s net zero objectives. The initial reaction to such an event would be addressing the immediate need, i.e. “Where are we going to get gas from now?”. Once alternative sources have been sought, such a situation could in fact accelerate the transition towards net zero alongside promoting energy security of supply by reducing (or even eliminating) Europe’s heavy dependency on Russian gas through mass investment in the net zero transition.

Such a view has partly been expressed by the Estonian Prime Minster Kaja Kallas, who said in a recent interview; “This absolutely is the time to focus on renewable energy sources … but also on agreements regarding LNG to substitute the Russian gas”.

Alternatively, in the wake of the initial uncertainty brought on by a partial or complete loss of Russian supplies there could be calls for greater investment in new gas infrastructure and production to retain the use of gas as an energy source while Europe weans itself Russian gas. Such a move could instead delay the region’s net zero transition by prolonging the existing dependence on gas.

How Europe’s energy markets deal with this unprecedented situation and the crossroads at which they find themselves may well set the direction of the sector for years and decades to come.