Throughout the recent period of wholesale and supply market volatility, the government and Ofgem have remained committed to the default tariff cap and continued to highlight its benefits to customers in protecting them from rising energy prices this winter.

However, Cornwall Insight’s forecast of the default tariff cap for Summer 2022 is now £1,897 per annum for a typical domestic dual fuel customer, with this figure including our latest view of both wholesale market costs and non-energy costs for both gas and electricity. This compares to the current Winter 2021-22 cap level of £1,278 per annum, which was itself a record high, while our Winter 2022-23 forecast (which has yet to commence the formal price calculation period running February 2022 to July 2022 inclusive is £2,054 per annum.

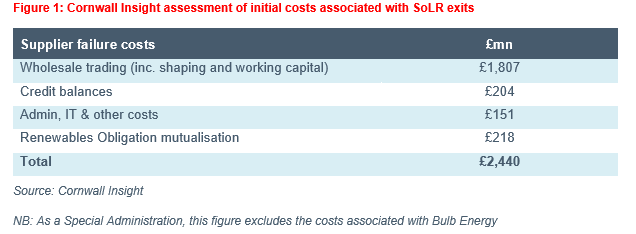

This includes our estimate of the costs associated with supplier exits over the period from September 2021 to December 2021 through the Supplier of Last Resort (SoLR) process, which stands at approximately £2.44bn. Of this, around 75% is in the form of wholesale energy purchase costs – this having already been given initial consent by Ofgem.

As we have discussed previously, the six-month nature of the cap serves to defer rather than eliminate any upward pressure on bills, which based upon the step change in the Summer 2022 cap is due primarily to wholesale cost increases. As such, there are a number of options going through the consultation process intended to mitigate this increase and re-establish stability to the market, but we note that there are other elements to consider:

- What happens if the wholesale market slumps?

- The future of Bulb Energy

- The non-domestic market

Log in or create a free account here to continue reading.