With more models entering the Australian car market and high prices at the bowser, electric vehicles (EVs) are garnering more attention from both cost-aware and environmentally conscious consumers alike.

In this context, AEMO’s forecasts predict a not-too-distant future where EVs outnumber combustion-driven vehicles. In fact, in AEMO’S 2022 Integrated System Plan (released 30 June 2022), EVs are expected to overtake internal combustion engine (ICE) vehicles by 2038-39. This will be a significant factor in shaping Australia’s future energy systems and markets.

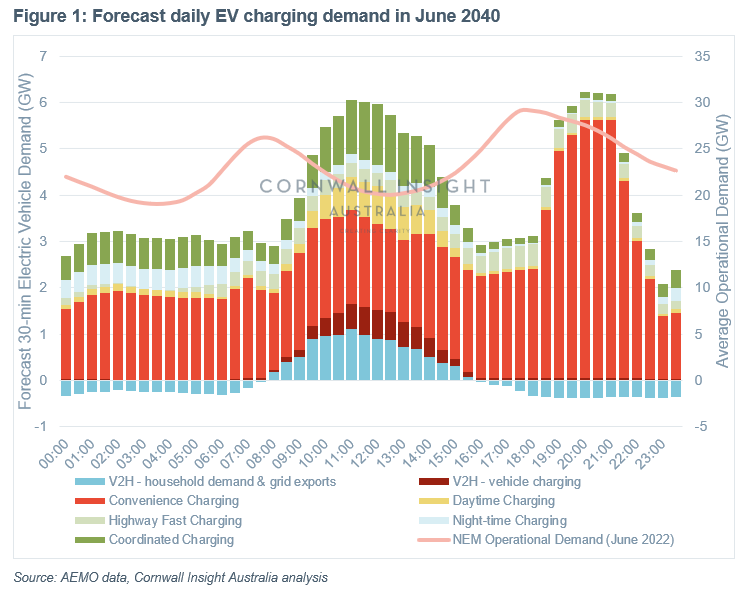

This week’s Chart of the week looks at the expected daily demand profile for EV charging across the NEM in 2040, based on projections for trends in EV usage and charging behaviours, in comparison to the daily NEM operational demand profile for June 2022 provided for context.

Particularly noteworthy from the above chart is the two roughly equally-sized peaks in EV demand – the first of which occurs in the middle of the day and coincides with the solar PV generation peak, where EVs can make use of abundant renewable energy supply (and likely low wholesale energy pricing). The second peak between 7pm-10pm is likely to be more consequential in terms of impacts to the operation of the grid, as it seeks to heighten the ‘head of the duck’ curve (the peak in the pink Operational Demand line).

The demand forecast is divided into several charging modes or profiles, which are each defined by considering an anticipated usage pattern of the EV and motivation for plugging it in:

- Convenience charging, where the EV is plugged in at times most convenient for the user, typically in the evening after use during the day (such as returning home from work). In 2040, the aggregate demand from this charging profile will be around 2GW during the morning and day hours, spiking to around 5.5GW in the evening peak. This evening peak would equal 19% of the peak operational demand for June 2022 for comparison.

This is the primary charging mode in AEMO’s projections for the next 15 or so years, with a 90% share in 2022-23. AEMO forecasts convenience charging to reduce to 47% in residential settings by 2039-40 but remain high at 76% for commercial and industrial EV use. While this may be the most practical mode for the general consumer, it will likely exacerbate evening peak demand issues; - Night-time & daytime charging, where the user selects to predominantly (but not exclusively) charge the EV at particular times. An example of this would be a residential EV owner with solar panels typically using daytime charging, but occasionally requiring a night top-up before a long trip. Use of these modes will peak around 2033-34 before network-coordinated charging starts to take over;

- Highway fast charging, where EVs on long trips are connected to roadside fast-charging infrastructure for top-ups. This mode sees utilisation throughout the day in high-demand short-period bursts, but the use of this mode is inherently limited by its location-specific nature (in the middle of travel routes rather than at the ends), and typically has higher costs per kWh delivered;

- Network co-ordinated charging, where EV chargers are controlled by distribution networks to avoid use during periods of high demand. This mode is forecast to pick up from FY26 and take share from uncoordinated daytime/night-time charging as well as convenience charging. The typical daily demand profile of co-ordinated charging is not provided in AEMO’s reports, but for the purposes of the Chart a 50:50 mix of the daytime and night-time charging modes is assumed, both avoiding evening peak demand;

- Vehicle-to-home (V2H) and vehicle-to-grid (V2G) bidirectional flows are not expected to be significant until after 2030-31 as vehicles supporting these modes become more readily available on the market and as technologies mature to promote their integration with distribution electrical infrastructure. By 2039-40, these profiles each take up around 7% usage share when EVs are charging.

The V2H/V2G modes act in opposition to the peaks and troughs of the duck curve to smooth the daily demand profile. This effect can be seen in the chart where there is a consistent ~200-250MW of negative demand through the night. The driver of this behaviour is economic – the EV battery will have charged using cheaper energy from the daytime, when solar output is high and wholesale prices are lower, so it will be more cost-effective for the consumer to utilise this energy to power their homes through the night.

While 2040 is a long time away, such an increase in evening peak demand may cause headaches for network operators and planners if this view of EV charging behaviour becomes a reality. An alternate mitigation strategy could focus on avoiding the ‘convenience charging’ peak in the first place, with clever use of timers and smart chargers (both of which are already available on the market) to shift and spread the demand through the night, and to coordinate charging with renewable energy output.

Cornwall Insight Australia will continue to explore the implications of AEMO’s 2022 ISP going forward, including through updates to our Benchmark Power Curve. For more information, please contact enquiries@cornwall-insight.com.au.