Thirty-one retailers have gone bust since the start of 2021 in the UK. At least one of those entities has a subsidiary in the Australian market (having yet to acquire any customers, according to the most recent AER and ESC data). In this Chart of the week, we take a look at the growth of the retail market in Australia and whether there has been any meaningful change in market share from new retailers over the past decade.

For this analysis, we have considered new retailers to be those that have entered the market after 2012. The total number of new retail licences granted by the AER since 2013 (incl.) is 69, which is more than a doubling of the roughly 40 licences that had been granted as of the end of 2012; in 2019 and 2020 alone the AER approved 25 new licences (14 and 11 respectively). Over the last 9 years, this represents 12.2% compound annual growth in the retail sector. However, of those 69 who have received retail licences, only 40 of them have acquired a customer (based on the AER and ESC data). To give context for the UK, 13 additional retailers were entering the market in 2016, 18 in 2017, 4 in 2018, 8 in 2019, 2 in 2020, and 2 in 2021 (as at Q3).

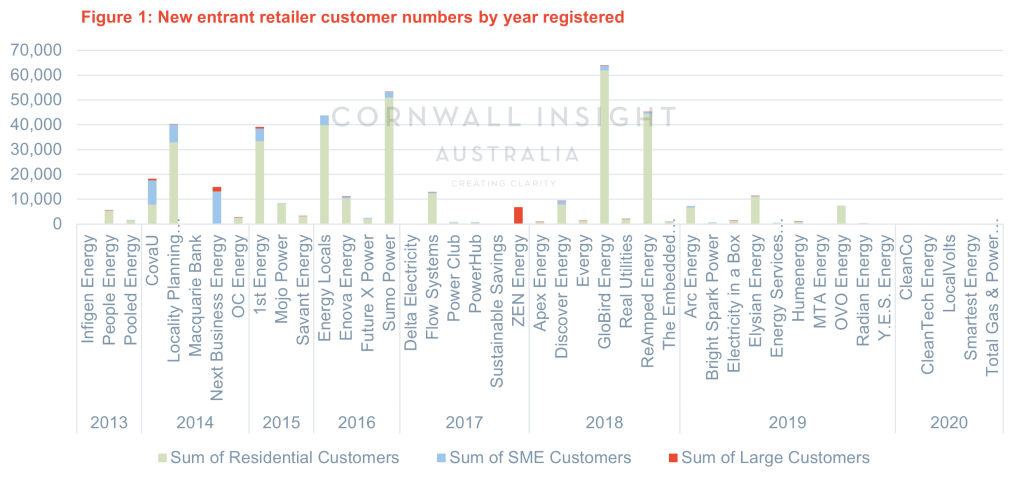

Below is a graph of the current number of customers that each of the new entrant retailers services, broken out by the year their retail licence was approved. Interestingly, a significant number of these new entrant retailers have failed to acquire a significant number of the customers, with only 5-6 of them having acquired more than ~40,000+ customers. Meaning that less than 10% of these new retailers have had any real impact on the market. As a total share of the entire retail market (by customer), they have only acquired 5.9% of customers, mostly in the residential space. The latest retail report from the AER states that the Tier 1 retailers (or the primary regional retailer) account for more than 80% of the residential market. This remains relatively unchanged even though we have switching rates across the NEM ranging from 3.5% in SA to 6% in VIC (when adjusted for AGL’s acquisition of Amaysim Energy in late 2021), meaning that much of the switching that is occurring is between the bigger retailers.

Ovo Energy (which, after having acquired one of the largest retail books in the UK, became the second biggest retail supplier with over 5million customers in 2020) but prior to this grew over a decade to have ~1.5million customers. For context, the UK has around 28 million customers, meaning they acquired ~5.3% of the market. Ovo has a retail licence in Australia and launched in 2019, but has only managed to acquire ~7,500 customers, roughly ~0.1% of the Australian market in 3 years. Bulb in the UK was founded in 2013 and grew to 1.7 million by the end of 2021 (before going bust in part to rising gas prices and insufficient hedging strategies), but during that period, it was able to acquire a significant portion of the market within a relatively short period of 8 years. This ability to capture market share appears to be a significant barrier in the Australian retail market. Even the largest new entrant retailer GloBird Energy has only acquired ~62,000 customers, which is only ~1% of the market.

It appears that we have a significant problem in the Australian retail market that even with a significant number of new entrants that have extremely promising business models that deliver value to customers, they have as yet not managed to convert those into customers switching from the large retailers. Additionally, the current ISP has more than 30GW of controllable DER/Storage to be leveraged from customers being a part of the wholesale market by 2050, but at this rate, it does not appear that we have sufficiently innovative tools or sufficient customers aligning with new retail models to be able to capture and realise that DER based future.