In 2017, the Victorian Government legislated a state target of net-zero greenhouse gas emissions by 2050. Since then, short-term targets have been set in five-year increments, with the 2030 target being to cut emissions by 45-50% below 2005 levels. The Government is currently consulting on the 2035 target, which must be set by March 2023. It will likely put forward an updated climate change strategy, along with whatever target it chooses for 2035.

While reaching net-zero emissions is about the whole state economy, including transport, heat, industry, and non-energy emissions, the reality is that decarbonising the electricity supply lies at the heart of most credible climate strategies. For example, a key enabler of achieving the 2030 target is the closure of the Yallourn brown coal power station in 2028 and its assumed replacement with lower emissions alternatives.

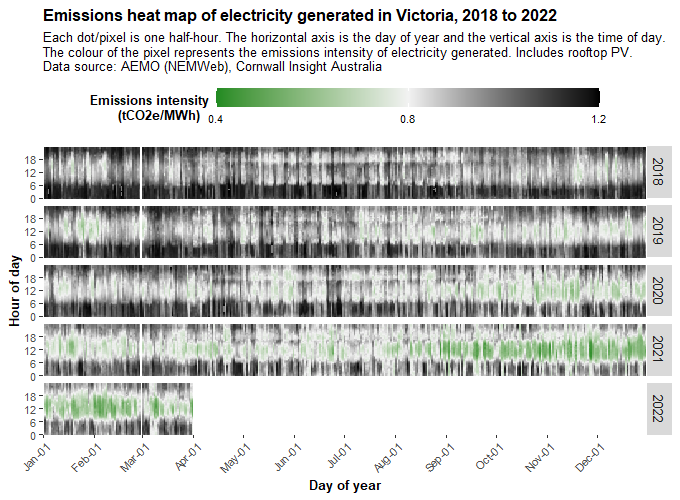

In this Chart of the week, we look at the half-hourly emissions intensity of Victorian electricity supply over the last few years to evaluate progress so far. First, the headline numbers – annual emissions intensity has fallen from 0.97 tCO2e/MWh in 2018 to 0.83 tCO2e/MWh in 2021 and 0.81 tCO2e/MWh in 2022 year-to-date, representing a 16% reduction in the emissions intensity of electricity supply. The Chart below shows that the bulk of this improvement has come during daytime hours, primarily due to the uptake of rooftop solar PV by homes and businesses, and partly due to utility scale solar. Emissions intensity in the evening and overnight has improved too thanks to an influx of wind capacity, but not as markedly as the middle of the day. Seasonal effects are somewhat noticeable too, with emissions intensity in spring and summer being lower than in winter (although a comparison between months within any one year is affected by new supply coming online throughout the year).

Going forward, it appears that the largest emissions benefit would come from targeting periods outside daytime hours, where intensities are highest. Of course, rooftop PV should and will continue to play a role in decreasing emissions, but the Chart shows that the marginal emissions benefit of each panel added in 2022 is considerably lower than in 2018. Furthermore, Victoria’s brown coal power stations are often regularly running close to their minimum stable level, indicating that only so much rooftop PV can be added before either the stations are retired, or rooftop PV starts being consistently curtailed.

Yallourn’s closure is already slated for 2028, creating “room” in daytime hours for more solar and rooftop PV and helping to meet the 2030 emissions target. But what about meeting the upcoming 2035 target? We don’t know the target yet, but if we take a roughly linear trajectory towards net-zero by 2050, we can estimate the target will be an emissions cut of 60-65% relative to 2005 levels. The electricity supply will need to do much of the heavy lifting again. Much of the low hanging fruit (rooftop PV) will be exhausted by that time. The Victorian Government’s recently announced offshore wind targets will help decrease emissions in the evenings and overnight, but it looks increasingly likely that another brown coal power station also needs to go.

Cornwall Insight Australia’s in-house Benchmark power curve price forecast subscription services shed light on how prices are likely to evolve, considering the impacts of new regulations. For more information, please contact us at enquiries@cornwall-insight.com.au.