Last month, the Australian Competition and Consumer Commission (ACCC) announced that there will be a gas shortfall in the east coast market in 2023, not a surprise considering the international gas crisis and high gas prices in Australia. Such events have increased attention towards expanding gas supply or reducing the gas demand in Australia and worldwide.

One well-known alternative for reducing natural gas demand is hydrogen. In this regard, polymer electrolyte membrane (PEM) electrolysers are expected to become an important part of hydrogen production in Australia. PEM electrolysers consume electricity to produce hydrogen.

Although PEM electrolysers are on the top of the list regarding hydrogen production, they are subject to an operational limitation: the price of electricity they consume. This means the employment of PEM electrolysers can quickly become non-viable if the electricity prices are high. To reduce this risk and increase “green” credentials, PEM electrolysers can be coupled with renewable energy sources and/or a battery energy storage system (BESS). However, adding a renewable generator or a BESS to a PEM electrolyser business case increases the project’s capital expenditure.

In this Chart of the week, we investigate if a BESS can add viability to a PEM electrolyser by levelling its exposure to high electricity prices during the day.

We have conducted a simulation where an electrolyser with 10MW of electricity consumption is coupled with a BESS, both connected to the grid. The analysis uses electrolyser costs similar to AEMO’s 2020 ISP FY22 capital cost of $3500/kW and an estimated project lifetime of 20 years. The operation cost includes the maintenance cost, and the cost of electricity with the electrolyser assumed to run at an 80% capacity factor (which has not been finely optimised on pricing vs capex). Electrolyser’s efficiency is 73% (54 kWh/kg H2), and the WACC has been considered at 10%.

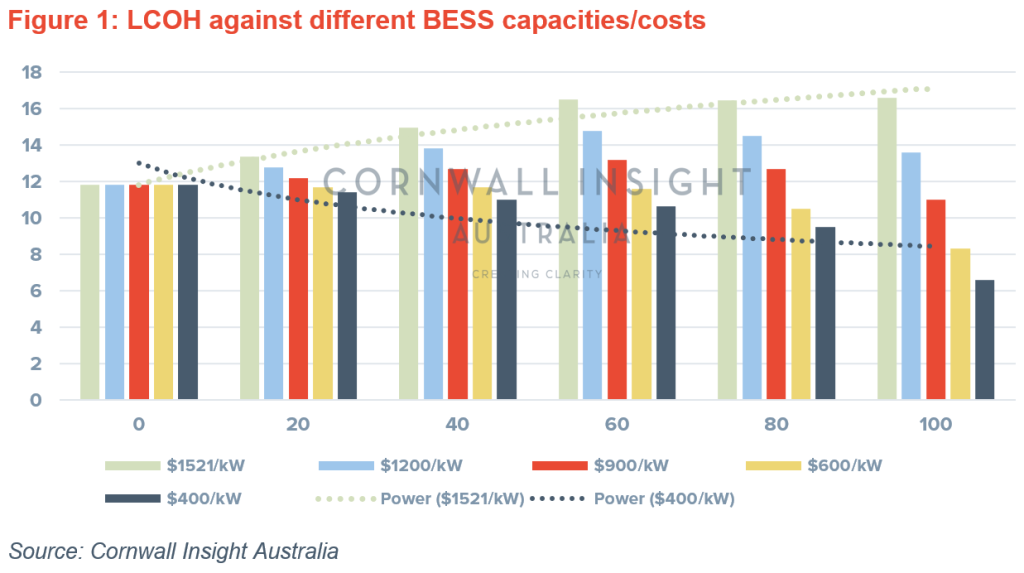

The levelized cost of hydrogen (LCOH) has been given in the chart for different BESS capacities (MW) and BESS capital costs ($/KW). The cost of BESS has been considered in a range from $1521/kW (including registration fees) to $400/kW to reflect the future changes in BESS capital costs.

As is seen in the chart, with the current capital cost of BESS and the electricity prices in the NEM, a BESS cannot add viability to the PEM electrolyser (see green bars). The reason is that while a BESS can reduce the electrolyser’s exposure to high prices, the BESS capital expenditure results in higher values of LCOH. Note that this only shows the LCOH for a BESS coupled with a PEM electrolyser (a large load to be supplied by the grid and possibly the BESS) and DOES NOT mean that a standalone BESS is an infeasible project on its own.

Assuming the cost of BESS is reduced to 600-400 $/kW (forecasted in 2040-2050), a BESS coupled with a PEM electrolyser is more viable than a standalone PEM electrolyser. This is shown with the dark navy bars in the chart.

To conclude, a BESS can add viability to a PEM electrolyser and can reduce the LCOH, but this is only true if the capital cost of BESS considerably reduces to $900/kW for large-scale BESS (almost 100MW) and to 600-400 $/kW for smaller sizes. The size of the BESS is of importance here as the bigger the BESS, the less exposure to high prices by the electrolyser (let’s not forget that the electricity price is an important element in determining the LCOH).

It should also be noted that the cost of electrolyser is also projected to reduce to almost $1000/kW post-2030. However, this does not reduce the LCOH as we may expect, but the $2/kg hydrogen is not a dream if the electricity prices cooperate too.

In this study, we benefited from our benchmark price curves which provide a high-resolution forecast of electricity prices in the NEM to 2050. For more information on our benchmark price curves, please contact us at enquiries@cornwall-insight.com.au.