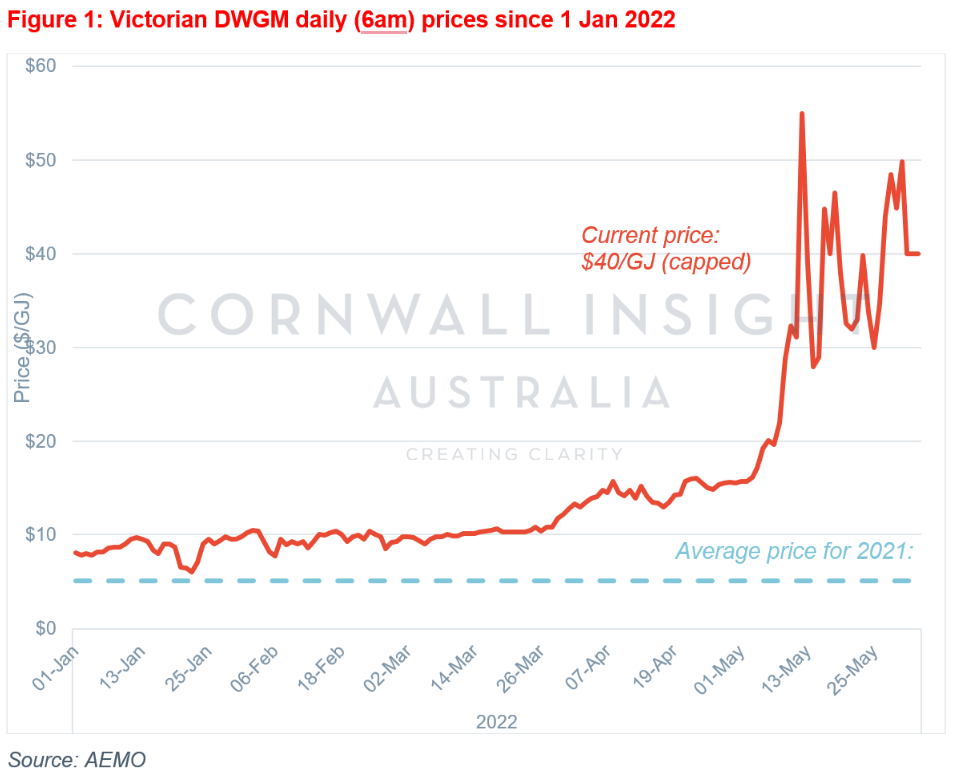

Australia’s gas markets are in the middle of an unprecedented price spike. Current prices in the Victorian Declared Wholesale Gas Market (DWGM) have been tracking in the $20-40/GJ range since early May 2022, with prices hitting $50/GJ on 30 May. Prices in the other gas hubs of Sydney and Brisbane are also regularly around the $30/GJ price range. By comparison, the DWGM averaged $5.10/GJ last year.

While price spikes like this have occurred in the past, these usually only last a day or two before settling to more normal levels. This current spike has been sustained for weeks, which has never been seen before in the gas wholesale market. In fact, AEMO (the market operator) has started capping the DWGM price at $40/GJ to prevent the price from further blowing out.

There are many reasons behind the spike:

- The Russian invasion of Ukraine means Europe is urgently seeking non-Russian energy supplies. This results in Australian LNG filling gaps in this changing global supply chain. Namely, Asia will be seeking more LNG from Australia as other countries divert their supplies to Europe. Domestic prices have risen as export prices become more appealing.

- Numerous outages at coal power stations also mean increased utilisation of gas-fired electricity generation, increasing the demand for gas.

- Cold weather also increases the demand for gas for heating, especially in Victoria.

Highlighting the fragility of the market, AEMO declared that there not be enough gas available for Victoria, South Australia, and Tasmania on 2 June 2022, although AEMO appears to have resolved this.

The high gas wholesale prices have had one casualty already, with gas retailer Weston Energy having their retail licence revoked as they could not meet the high prudential payments deriving the burgeoning wholesale price. Commercial and industrial users on wholesale pricing contracts will also be feeling the pain currently. Furthermore, as more gas-fired electricity generation runs, higher gas input costs have contributed to high spot electricity prices.

Yet the price spike isn’t the full story. Most gas users are on fixed-price contracts, so the spike effect won’t flow through for most customers yet. However, if the spike continues to be sustained, it is feared to be only a matter of time before the increases flow through to new gas contracts. Considering many large gas users will be coming off prices in the $6-10/GJ range, new gas contract prices closer to $15-20/GJ will send many businesses to the brink.

To alleviate the impacts of these high gas prices, there are calls for the new Federal Government to trigger the ‘Australian Domestic Gas Reservation Mechanism’ to reserve some supply for domestic rather than export purposes. It is unclear whether triggering this mechanism would alleviate the current spike, as according to new energy minister Chris Bowen, the trigger would not take effect until January 2023 anyway. Likewise, it is also unclear whether the trigger could even be executed under the current rules, as the trigger concerns supply, not price. Either way, the gas price spike presents a thorny issue for governments, businesses, and industries to solve.

For more information, please get in touch with us at enquiries@cornwall-insight.com.au.