AEMO has recently published the 2022 Integrated System Plan (ISP), which provides an energy transition roadmap for the National Electricity Market (NEM). This ISP focuses on the “Step Change” scenario, which reflects strong action on climate change leading to a step change reduction of greenhouse gas emissions, based on the stakeholders’ view of accelerated decarbonisation in the NEM.

As part of the process for the 2024 ISP, AEMO has started reviewing previous assumptions and scenarios. AEMO’s review of last year’s assumptions finds that the Step Change scenario will lead to less net emission compared to the Nationally Determined Contribution (NDC) – a carbon emission reduction target recently increased to 43% emission reduction on 2005 levels by 2030.

As part of sensitivity testing of our Benchmark Power Curve, we wanted to test what generation would be needed if Victorian coal retirements accelerated earlier than the Step Change scenario’s retirement schedule – refer to Figure 1 below:

Figure 1: Coal power station retirement schedule: Step Change scenario vs Accelerated scenario

| Coal power station | Step Change schedule | Potential accelerated schedule |

| Yallourn | 2025 – 2026 | 2024 |

| Loy Yang A | 2028 – 2030 | 2027 |

| Loy Yang B | 2032 | 2030 |

In this Chart of the week, we conducted a sensitivity analysis using AEMO’s ISP market model to see how the market would be able to replace the accelerated coal power plant retirement and how much emissions from power generation are reduced. Only the coal plant retirement schedule is adjusted in the ISP model in this study. The simulation focuses on finding the least-cost solution for the generation capacity that needs to be built to satisfy long-term capacity reserve and generation requirements.

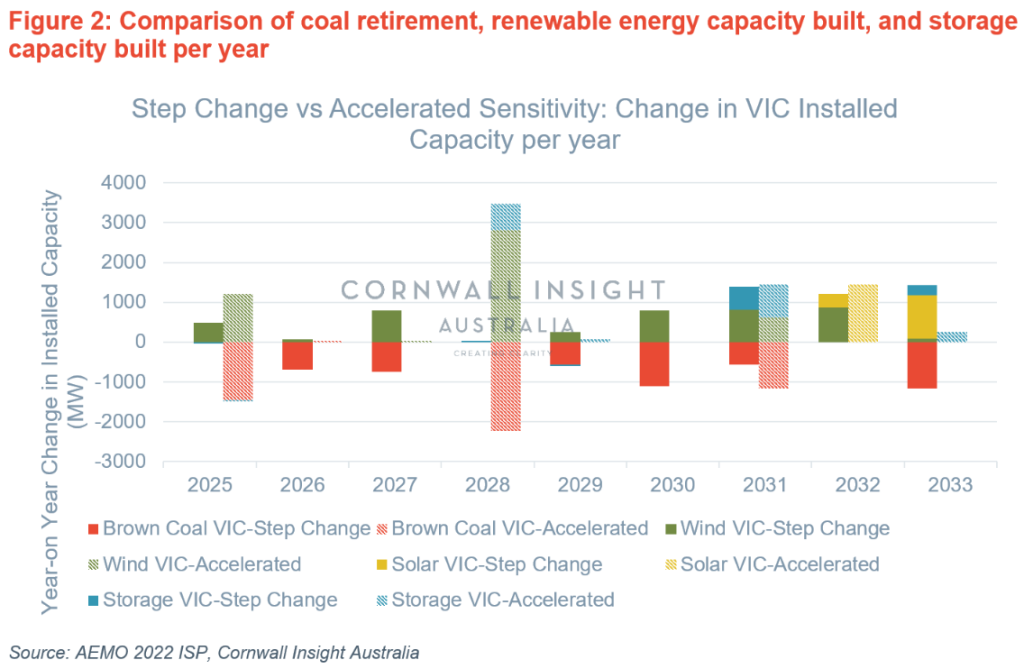

From the results of the study, the following chart shows how much renewable energy capacity and storage needs to be installed in Victoria to replace the coal power plants retiring at an accelerated pace. The negative numbers, particularly for coal power plants, represent the amount of capacity retired compared to the previous year, while the positive numbers represent the capacity built to replace the retiring capacity.

Based on the results, the accelerated schedule of the retirement of coal power plants will require building approximately 4000 MW of wind capacity (including about 600 MW of energy storage) by 2028 compared to only about 13S00 MW of wind capacity in the Step Change Scenario to meet system needs. Since the retiring coal power plants are to be replaced by renewable energy capacity, a significant amount of energy storage needs to be built to satisfy the generation requirement, particularly during the evening peak periods. In the ‘Accelerated Scenario’, about 1800 MW of storage needs to be built by 2033 compared to only about 830 MW in the Step Change scenario. It might be a challenge to build this much capacity in a single year to replace the retiring coal power plants; however, spreading out the retirement across multiple years, similar to the Step Change scenario schedule, may help.

Aside from generation coming from new capacity, the accelerated retirement schedule will also introduce changes in Victoria’s imported energy. In 2028, when Loy Yang A retires in the ‘Accelerated Scenario’, about 4800 GWh of imported energy is required – 4000 GWh more than in the Step Change scenario. In 2032, when VNI West (Keranglink) is planned to be operational in the Step Change scenario, about 3500 GWh of energy will be imported compared to the 1000 GWh of import in the Step Change scenario.

As VNI West is also expected to increase hosting capacity in Western Victoria, it may be prudent to move its commissioning date one year earlier in preparation for the accelerated retirement of Loy Yang B.

Shifting coal plant retirement will lead to about an 11% reduction in net emissions coming from electricity generation by 2031 (after Loy Yang B retires in the ‘Accelerated Scenario’) for the whole NEM in the Accelerated scenario compared to the Step Change scenario. This would require a significant amount of renewable energy and storage capacity to be built in Victoria, which is no easy task. Spreading out the retirement of the Loy Yang unit across several years while building interconnectors earlier will definitely make that transition ‘easier.’

Cornwall Insight Australia largely uses AEMO’s ISP assumptions in our Benchmark Power Curves (BPC) subscription and other market modelling services. For more information, please contact enquiries@cornwall-insight.com.au.