The number of thermal generator problems continues to grow, and so does peak time volatility in the two northern states. On top of the closure of Unit 3 at Liddell occurring on 1 April and Unit 4 at Callide C still out without a public resolution, outages and problems have been seen recently at a host of other coal stations: Unit 5 at Vales Point B – with a generator fault and hydrogen leak taking out one of its two 660MW units for more than a month; Unit 2 at Loy Yang A – which was taken out of service due to an electrical fault with the generator; and Gladstone – which has experienced fault issues recently and has submitted Unit 3 for a long-term outage: have all contributed to the growing injury list in recent months.

The outages are linked to being one of the major reasons for the large spike in prices seen in the first four months of the year. High prices, particularly in the evening ‘super-peak’, have become increasingly apparent as the NEM’s bimodal pricing accelerates – and these peak pricing events can cause serious damage to the market for retailers.

Coal capacity utilisation has told an interesting story post pricing events, but given that we are now traditionally heading into the time of year when solar and wind output drops, are there any particular days in the upcoming period that could spell further trouble? This Chart of the week explores the submitted max outputs for coal generators for the next three months, where the text will focus on a few key dates where possible trouble may occur.

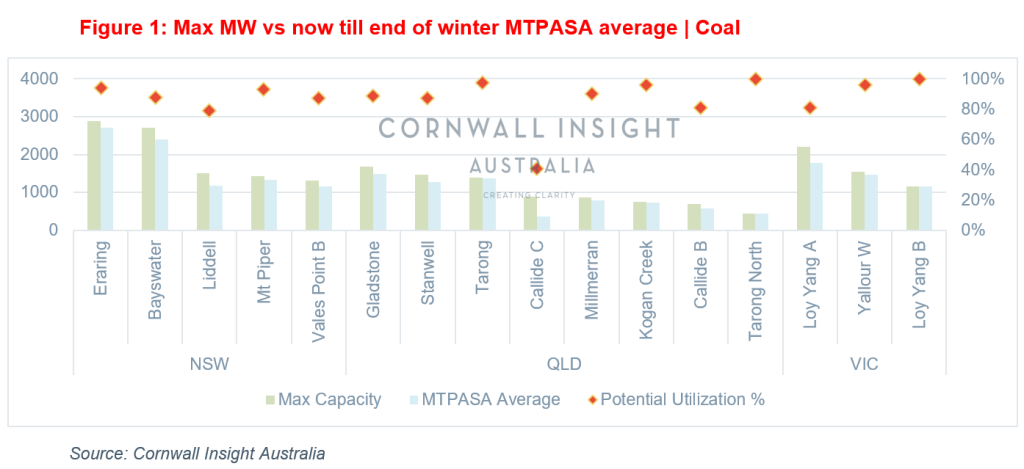

The following figure shows the average coal capacity output in MW over the past 30 days compared to the maximum capacity of the generator.

Given the increase in prices over the last few months, of which a large proportion is caused by the increase in the spot gas price, the potential for continued high prices and cap prices ($300/MWh) remains high; however, it is exposure in peak times that may look worrying during the cold, cold winter.

Given that Queensland has a poorly diversified power generation system and the coal generation has struggled to ramp high enough in the evening peak, the below table highlights a few dates that should be kept in mind over the next few months.

April saw QLD average a spot price of $220/MWh and NSW $187/MWh, driven by the increase in gas price and coal outages. QLD peak time was the most worrying, with an average of $759 in the 6pm-7pm timeslot. Given the uptick in prices, it was no surprise to see that the QLD spot price was set by black coal generators at just over 65% for all dispatch intervals this year – something that will likely remain going ahead for the short term.

An interesting event occurred on 1 February, where scheduled outages in QLD saw three Units (Callide C Unit 4, Kogan Creek, and Callide B Unit 2) out of the 22 go offline with outages. In turn, this saw the average price rise to $1607/MWh for the day, largely boosted by the amount of periods exceeding $10,000/MWh.

Prices have also spiked over the last few days with Gladstone reduced to half, Callide C completely out, and Milmerran missing a unit – the 9th wasn’t helped with shortfall across all four mainland states.

Days to watch will determine whether MTPASA reports can give an accurate picture of the wholesale price for certain days, with QLD having a few coming up, and you may expect some heavy prices from the 27 to 30 May with MPP1, GSTONE3, and CALLB2 off. This scenario will be repeated from 26 till 30 June. NSW is going through a similar scenario now until 12 June with elevated prices due to BW01 and BW03, ER4, LD1, and MP2 outages leaving a gap of over 3250MW.

Our Energy Market Perspective may be of interest for more information on price trends and energy balance figures. Get in touch for more information. For more information, please get in touch with Cornwall Insight Australia via enquiries@cornwall-insight.com.au.