At the end of January we released our latest Green Power Forecast, projecting renewables generators revenues over a five-year horizon whilst also providing Power Purchase Agreement (PPA) pricing and benchmarking updates, and a survey to gauge the latest renewables market trends.

Amid the current “energy crisis” arising from an underlying rise in wholesale prices, forecast renewable generators’ revenues have risen significantly. However, the ramifications of the current crisis are far-reaching, with PPAs being no exception.

In this blog we explore some of the latest trends in key revenue streams for renewables assets.

Wholesale prices up significantly, but cannibalisation impacts loom

Wholesale power contracts rose considerably over Q421 (October – December), where seasonal contracts out to winter 26 lifted ~25% on average. Gains in wholesale prices were most pronounced in nearer-term contracts: contracts for near-term delivery saw the largest increases, with the summer 22 contract up nearly 70% quarter-on-quarter, and the winter 22 contract trading in excess of 70% higher.

Power contracts have risen due to record high gas prices in the so-called energy crisis, in conjunction with strong performing underlying commodity markets (such as LNG and carbon prices), and a trend of low wind and renewable generation during the quarter.

Despite these highs, price cannibalisation—the depressive influence on the wholesale electricity price at times of high output from intermittent weather driven generation such as solar, onshore, and offshore wind—continues to affect the captured wholesale price of wind and solar technologies.

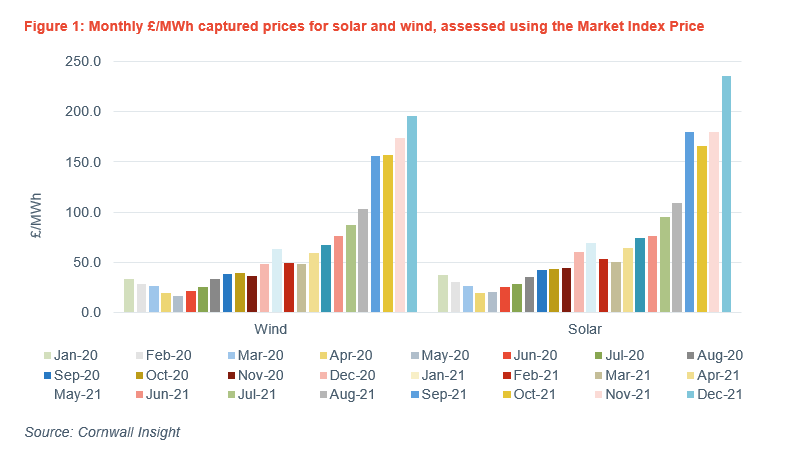

Captured prices in Q421 achieved by wind technologies averaged ~8% below baseload prices (assessed using the Market Index Price), while solar PV prices instead averaged 1.2% higher than baseload prices in the quarter, buoyed by its daytime generation profile. Nonetheless, the recent surge in wholesale prices saw solar PV and wind captured prices (i.e. absolute £/MWh values) in Q421 rise notably, once again breaking records in our analysis since January 2015. Figure 1 below shows the monthly captured price for wind and solar technologies between January 2020 and December 2021, with the impact of the surge in wholesale power prices hard to miss.

Roc prices are trading at elevated levels, whilst FiT generators enjoy option to switch

Generators accredited to the Renewables Obligation (RO) scheme have also benefitted from healthy forecasts of Roc values, at least for the near future.

Traded Roc values in the current compliance period (CP) CP20 (2021-22), have risen in light of low wind output persisting across most of the year. For CP21 (2022-23), the RO target being set at the second highest level has also benefitted RO-accredited generators, resulting in expectations of greater Roc demand from electricity suppliers, and therefore the potential for a high Roc recycle value to be realised.

Unlike other subsidy schemes, RO generators remain entirely exposed to volatile wholesale prices, and therefore the rise in wholesale power prices of late will be a welcome change from the extreme lows observed during the peak of the COVID-19 pandemic. However, the extent of any additional revenue from realised Roc values will ultimately depend on prevailing trends within any CP, such as renewable output and electricity demand levels.

Meanwhile, FiT generators have enjoyed their ability to switch between the administered export tariffs set by Ofgem, and a commercial PPA that includes prevailing wholesale prices and other sources of revenue such as embedded benefits. This is an annual choice, where the latest export rates have been set at £55.70/MWh (2021-22 money) or £39.50/MWh (2021-22 money), depending on accreditation date. As the front annual baseload power price remained markedly higher than both the lower and higher export rates during Q421, averaging £132.84/MWh, FiT projects were reported to be increasingly switching away from the administered export tariffs and onto commercial PPAs.

REGOs are trading at all-time highs

REGO prices have maintained a strong upwards trajectory in 2021 and into 2022, repeatedly breaking record highs across both fuelled and unfuelled technology types.

Increasing demand for REGOs, in part following low wind output across most of 2021-22 has supported prices for the certificates, particularly in the near-term; REGOs for the 2021-22 Fuel Mix Disclosure (FMD) period have reportedly traded in excess of £6/REGO in recent months. While it is generally expected that REGO prices for future FMD years will subside from the current highs, relatively high values have nonetheless been reported by market participants. This is starkly contrasted to traded REGO values prior to 2021-22, where values were rarely reported above £1/REGO, particularly during the initial stages of the COVID-19 pandemic when REGOs traded below £0.2/REGO at times.

While gains have been most pronounced in nearer-term FMD year REGOs, prices for later-dated REGOs have also risen, with prices further along the curve being buoyed by increased demand from corporates, who are increasingly using REGOs as part of their ESG reporting.

Our quarterly Green Certificates Survey explores certificate pricing trends in more depth, with the latest report issued only yesterday.

But PPA pricing has become more challenging

While forecast green generators revenues have risen, a welcome change compared to projections during the peak of the COVID-19 pandemic, the energy crisis has impacted actual achievable values for renewables sites. This impact is exemplified by the latest trends reported in the PPA market, as part of our conversations with market participants.

Against a backdrop of extreme levels of volatility in the wholesale market and in imbalance prices, alongside uncertain output levels and the impacts of price cannibalisation on intermittent asset types, offtake parties providing PPAs have had to adjust their offerings. This has made the job of pricing PPAs more difficult, ultimately resulting in reduced % value retention (against full market values) that generators are able to achieve in the market. Some market participants in our survey noted that offtakers found fixed-price PPA offerings particularly challenging, and are instead preferring to offer market-indexed PPAs. That being said, the reduction in % value retention levels in PPAs has more than been offset by the underlying rises seen in key revenue streams available to renewables, namely wholesale prices.

If you are interested in our Green Power Forecast report, forecasting a wide range of revenue streams available to renewables assets whilst also providing bench PPA pricing levels and a survey of trends in the wider renewables market, please contact b.bagge@cornwall-insight.com or t.ross@cornwall-insight.com.