“Q: How does 2pm on Wednesday sound? A: Assuming we still have a functioning energy market that’d be great”.

It’s not really what you expect to see in an email at 5pm on a Friday when trying to arrange a call. But then these are certainly not normal times. In this Energy Perspective, we will try to persuade the great and the good not to let competition in the retail energy market die amidst the carnage of a commodity storm.

Good bye to all that!

Wholesale gas, power and carbon prices have been a one-way bet since the turn of the year. Normally the British wholesale energy markets track lower through the summer, reflecting relief that the last winter did not turn out that bad and hope that next year will be like this year.

After lows driven by collapsing demand through COVID-19, prices have been surging upwards since the spring and have really accelerated through the summer (Figure 1). The media has focussed on the coming 10% or so increase in the Default Tariff Cap but amongst the first to feel the squeeze have been businesses. Manufacturers have been cutting production, with knock-on concerns about supplies of their products, meaning costs for those striking new contracts have rocketed.

Not far behind have been concerns about the stability of energy retailers, especially those in the domestic market caught between rocketing wholesale markets and the maximum prices of the Default Tariff Cap. Four smaller suppliers have exited through Ofgem’s Supplier of Last Resort (SoLR) mechanism in the last two weeks and there is a widespread expectation that more will follow, potentially many more.

A series of unfortunate events

How we got here has nothing to do with energy suppliers. Factors driving the storm include:

- Strong competition for LNG deliveries between Europe and Asia amid some outages at production facilities in the US. World LNG prices generally remain at a premium to high European market prices.

- A tightening of EU carbon market rules that has incentivised coal to gas switching by power generators even as wholesale gas prices have accelerated upwards.

- Outages in Norwegian gas supply, low Russian supplies with continued uncertainty surrounding the start-up of operations at Nord Stream 2, particularly as it awaits regulatory approval from Germany.

- Low gas storage levels ahead of winter across Europe. Britain has no long-range gas storage since the Rough facility closed in 2017.

- Closer to home, more British nuclear and gas power stations being offline than expected, lower than anticipated solar and wind output and, just last week, a fire shutting down a French interconnector.

Not all are products of the last few weeks. The implications for winter supplies were brought into sharp focus by National Grid ESO releasing “Our early outlook on winter margins in 2021-22” in July some three months before it would normally set out its view for the peak demand season.

Looking ahead, there do not seem to be too many factors that are likely to push down these prices. Indeed, it is not all about markets correcting through the effect of price. Some fear that gas supplies from Russia in to Europe are being slowed or withheld as Russia and the EU wrangle over regulatory control of the new Nord Stream gas pipeline.

These points bring home that the current crisis is one of resilience. The last 30 years have been a story of increasing globalisation and efficiency. Supply chains for gas stretch across the world and, as in many other industries, the logistical concept of “just in time” has become the key mantra. Costs have been cut wherever possible, notably in energy in Great Britain for gas storage. This has been a trend across the world and across industries.

This efficiency has come at a cost and has reduced resilience making us more reliant on key sources (including Russia for gas whether we like it or not as it is Europe’s marginal supplier) or supply links (interconnectors). Then we have had COVID enter stage left, which has interrupted our world and thrown our supply chains and the demand picture into chaos.

Politics enters through the front door…

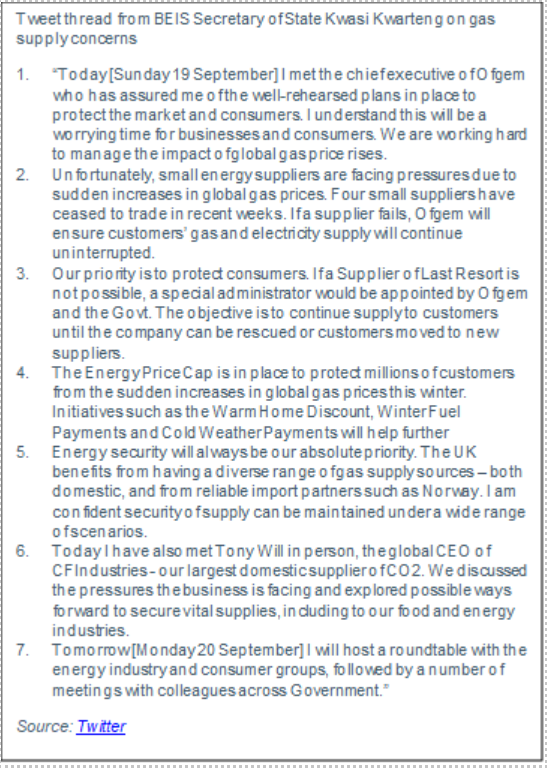

All the above made for a frenetic weekend (see Figure 2) leading up to a “roundtable” led by Business Secretary Kwasi Kwarteng looking to shore up supplies and, seemingly, the market structure itself. The Secretary of State’s tweets suggest some stark eventualities are being considered not least that more supplier exits are expected, with the possibility that there could be failures too big for other suppliers to digest through SoLR. It has also been suggested that there may be scenarios in which secure gas supplies may not be maintained. Whilst the focus of politicians is understandably on securing supply, we would say that one keen eye also needs to remain of securing competition too.

Competition has been synonymous with consumer benefit for a decade or more of energy regulation and policy. A functioning retail market with effective competition is an outcome consistent with Ofgem’s duties, as “wherever possible” they will fulfil their functions by “promoting active competition”. As recently as the summer, BEIS talked of a market in which energy suppliers “compete with a variety of business models, so that there is competitive pressure to continually improve quality of service and consumer choice” and where “consumer choice and active competition through the market will be the best approach to allow winning business models to grow”.

There are good reasons why these beliefs are held. New entrants have delivered considerable benefits—better prices from fixed tariffs, mass market greener tariffs, online prepayment, better service—which have all accompanied the wave of domestic market entry since 2014.

Whilst competition exits through the back door

But the immediate crisis threatens competition. With gas prices surging, energy suppliers have found themselves vulnerable to increasing prices. Retail offerings are being pulled or surging in price. It is very apparent that energy supply this winter is likely to be loss making; so many trading counterparties are withdrawing and reducing liquidity further. Some smaller suppliers have had their trading deals redrawn or even pulled leaving them even more vulnerable to market changes.

Outside of the four recent failures, even some of the largest suppliers are scrambling for capital ahead of the winter, underlining that the main shocks are external. Weekend media reports cited Bulb seeking new investment with the company telling the BBC that “from time to time we explore various opportunities to fund our business plans and further our mission to lower bills and lower CO2”.

The characterisation of exits being down to bad practice by suppliers is not always appropriate. The Default Tariff Cap complicates things. Its introduction marked a managed departure from faith in competitive markets and choice in delivering on that outcome. It was a political choice ahead of an election to close down the difficult subject of energy bills because of a fundamental unwillingness to contemplate what those costs really were and how long they would last. It had some obvious issues in terms of responsiveness to wholesale prices, but it was implemented anyway. The result recently is that the amount a supplier can charge customers has not been covering the costs of supplying energy which means that the fair cost for energy that OFGEM was trying to encourage is actually well under the costs of supply. Although the rise in the level of the price cap is set to increase by £139 from October to reflect rising wholesale costs, bringing the average dual fuel bill to £1,277, this is still over £200 below the cost to supply the energy

It has also been challenging for suppliers to hedge in line with the way the price cap is calculated. Indeed, the cap interplays with persistently inadequate responses to issues and risks around wholesale market liquidity and issues of inability to transact or trade without costly collateral and fees. Not all suppliers that are suffering today are doing so because of “bad practice” on hedging. There are a wide variety of versions of what the “right” hedging strategy is, and many which would have ordinarily been considered in the realms of the credible and sensible will have been caught the wrong side of recent events. Moreover recent exits have been foreshadowed by the termination or degradation of wholesale trading contracts by counterparties who fear the cap will leave suppliers so far underwater that they will be unable to settle their obligations, thus creating a self-fulfilling prophecy.

Further, key industry change programmes such as smart metering and half hourly settlement, which were to underpin a more resilient and responsive supply market, have not delivered on their vision. Many suppliers were seeking a competitive advantage from these changes and had banked on them occurring in line with original timetables when they entered the market. We can understand the anger in many who have been forced from a market that failed to deliver the infrastructure they were promised when they invested.

Taken as a whole, there is at least a case that the politicians have contrived to make their own trapdoor for the entrants it once claimed to desperately want in the market. Content to praise the benefits of competition in a benign commodity market when prices are falling but washing their hands of responsibility for failure when prices are rising. In truth, vulnerability of the system can be apportioned between some market players and some politicians.

In any event, it appears we are heading for accidental and costly reconsolidation, accelerating what was already a theme of the retail market population shrinking. Scale emerges as a defensive strategy against price uncertainty and politicians and regulators take comfort in these players, even if they require some fairly major financial cushioning to take on more obligations. The briefings over the weekend suggest an attitude is prevailing where businesses should be allowed to fail, and that “failing businesses” should not be rewarded through bail outs. Fair enough, but as we have argued, this is perhaps an over-simplification. If Ofgem, BEIS and HM Treasury are prepared to fund extraordinary costs in the market, do we need to wait for companies to fail before taking action with the attendant destruction of business, economic value and livelihoods which results?

Are we really to let over a decade of hailing competition as a desirable outcome be for nought? If so, many will have missed this rather critical change in energy policy objectives. As with so many crises, calm thinking is required to ensure the cure is not worse than the disease.

Hear more on this topic tomorrow:

This Energy perspective was taken from our Energy Spectrum publication on 20.09.2021.

To hear more of our thoughts on this subject, join our Energy Spectrum weekly webinar tomorrow at 9.30am. Register here to attend: