National Grid ESO (NGESO) launched the Dynamic Regulation (DR) service on 8 April, with the first auction held at 14:30 on the EPEX auction platform. DR is the second new product that the ESO has introduced to manage frequency on the system, as the system operator introduces a suite of three new faster-acting response services to better meet the needs of a high-renewables grid.

As we see a growing capacity of intermittent renewables on the system, with renewables penetration regularly exceeding 50% during windy days, system inertia levels are falling and the ESO must manage increasing frequency deviations. In response, the ESO has introduced new dynamic frequency products which are procured closer to real-time (at the day-ahead stage) with faster-acting delivery.

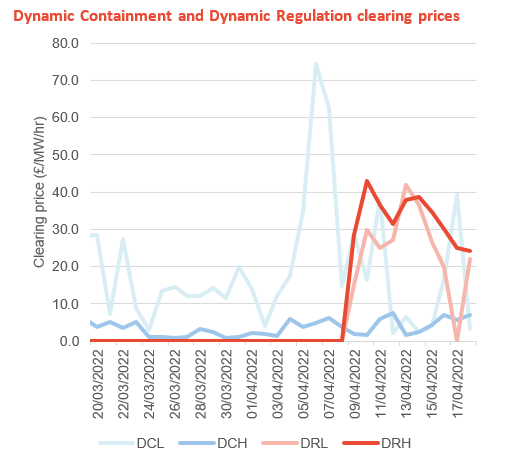

While Dynamic Containment (DC, launched in October 2020) and Dynamic Moderation (DM, first auction to be held on 6 May) require full delivery within a second, DR is designed with a slower delivery time of 10 seconds. DR is designed to slowly correct small continuous frequency deviations within ±0.2Hz of 50Hz, procuring downwards response to manage high frequency (DRH) and upwards response to manage low frequency (DRL) separately. Frequency is allowed to deviate within a small ‘deadband’ region of ±0.0.15Hz, before DR will be triggered. Given the small frequency trigger, DR will have the highest levels of utilisation. DR providers do not need to respond as rapidly as the other dynamic products, but assets must have a duration that supports continuous operation. We expect that providers who currently participate in the FFR market will be eligible to provide DR.

Analysing the first 11 days of auction results, we have seen four assets tender in from four separate providers (Tesla, Open Energi, Arenko and EDF). All are battery storage assets, which are active in DC and optimising across the two dynamic services. There has been a total of 329 bids accepted across DRH and DRL, with 78% of all bids successful.

We’ve seen volume dominantly procured in the DRH service, with an EFA-block average of 27.1MW procured, compared to an average of 10.3MW per EFA period for DRL. Prices have also averaged higher in the DRH service, averaging £27.1/MW/hr, six-fold higher than average DCH tender prices. Meanwhile, DRL prices averaged £27.1/MW/hr, enjoying a 72% uplift on its DCL counterpart. Once we see greater participation in the DR auctions we expect tender prices to fall, as previously observed when the DC service became oversubscribed.

The ESO has indicated that DR service requirement (along with DM) will be capped at 100MW while the new products are onboarded, for around 6 months, before we begin to see a gradual phase-out in procurement of the legacy Firm Frequency Response product.

Cornwall Insight’s Flexibility markets service offers complete coverage and insight across the GB electricity flexibility markets. Our comprehensive service offers regular price and value monitoring and forecasting of key revenue streams, highlights and explains important policy and regulatory changes and provides an independent view on the market landscape and competitor developments. For more information please visit our website here or get in touch with Tom Ross on t.ross@cornwall-insight.com.